Getty Images

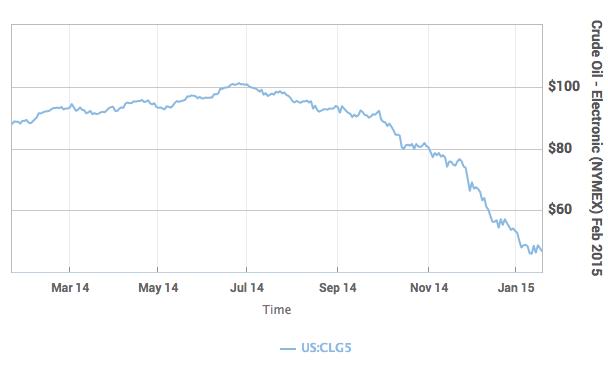

Getty ImagesSome argue that the oil prices have entered a new range of $20 to $60 per barrel. Others see the fall as temporary, seizing the opportunity to purchase assets cheaply.

Saudi Arabia and OPEC are unlikely to adjust production significantly. Oil minister Ali al-Naimi has pointedly stated that Saudi Arabia will not cut production even if oil prices CLG5, -3.96% fall to $20 per barrel. It is a historical shift, emphasizing market share rather than high prices, by controlling supply. Underlying the strategy is the focus on allowing low cost, efficient oil producers to increase their market power.

As the world’s largest crude oil exporter, Saudi Arabia is well-placed to implement this long-term strategy. It commands 25% of the world’s oil reserves. It has invested to maintain 2 million barrels per day spare capacity (over 80% of global spare capacity). It also has about $900 billion in foreign assets, giving it the wherewithal to survive significant revenue declines from lower oil prices for an extended period.

One constraint to the Saudi strategy is political. Lower prices damage U.S. shale gas and oil producers, and the complex politics of the Saudi-U.S. relationship will dictate managing the market share of shale oil rather than eliminating it completely.

In the present low-price environment, investment in more expensive or marginal projects will be delayed. Lower production costs can allow for further price declines. The ability to absorb low oil prices is not infinite, but based on past cycles the limits are large and have not yet been reached.

But price forecasts could easily be wrong. The structure of the oil market entails fine margins between demand and supply. The current oversupply is around 2 million barrels a day, less than 2% of global consumption. Price elasticity is also low, especially in the short run. Key uncertainties include weather conditions, unanticipated supply disruptions and geopolitical factors

An unusually warm or cold Northern Hemisphere winter that affects heating fuel demand has the potential to alter demand significantly. Refinery, pipeline, port, or other infrastructure breakdowns can affect supply. Weather conditions also impact production from facilities in Alaska, Canada and Russia. Accidents, such as recent Gulf of Mexico oil spills, can change the balance in the market rapidly.

Other political factors include actions relating to sanctions on Iran and Russia, and the civil wars in Iraq and Libya. One factor in the current supply glut was the increase of 800,000 barrels a day in Libyan production — a result of reopening export terminals following a truce between tribal militias in the civil war. This fragile truce is unraveling, with oil output dropping by around 400,000 barrels a day since September 2014. These factors have the potential to change supply significantly.

In the medium- to long-term, market forces, production costs and required economic rates of return on investment will assert themselves. Lower prices will increase demand and reduce supply. Investment losses will reduce production capacity, limiting the ability to respond to increases in demand. But these factors will take time to work through the market.

Moreover, several complications face the oil markets. Commodities, including oil, are generally traded in U.S. dollars. DXY, +0.15% The relative strength of the American economy and anticipation of normalization of interest rates is boosting the dollar. This may drive oil prices lower.

The global economy is experiencing disinflation and, in the case of some nations, deflation. Price pressures and a lack of pricing power in end-product markets affect inputs, such as oil prices, driving them lower. High interest-rates also result in lower commodity and oil prices. Interest rates are at historically low levels, near zero in many currencies. But the lack of inflation or deflation means the real interest-rate is frequently high, which drives oil prices lower. If these financial conditions persist, then the downward pressure on oil prices will continue.

Accordingly, in the near term, baring a sudden change in supply conditions, its seems probable that oil prices are likely to be weak, and volatile.

Satyajit Das is a former banker and author of “Extreme Money” and “Traders, Guns & Money.”

View original article here: http://www.marketwatch.com/story/crude-reality-oil-prices-are-going-to-stay-low-for-now-2015-01-20